27 November - Introduction

Nicolas Forest Chief Investment Officer

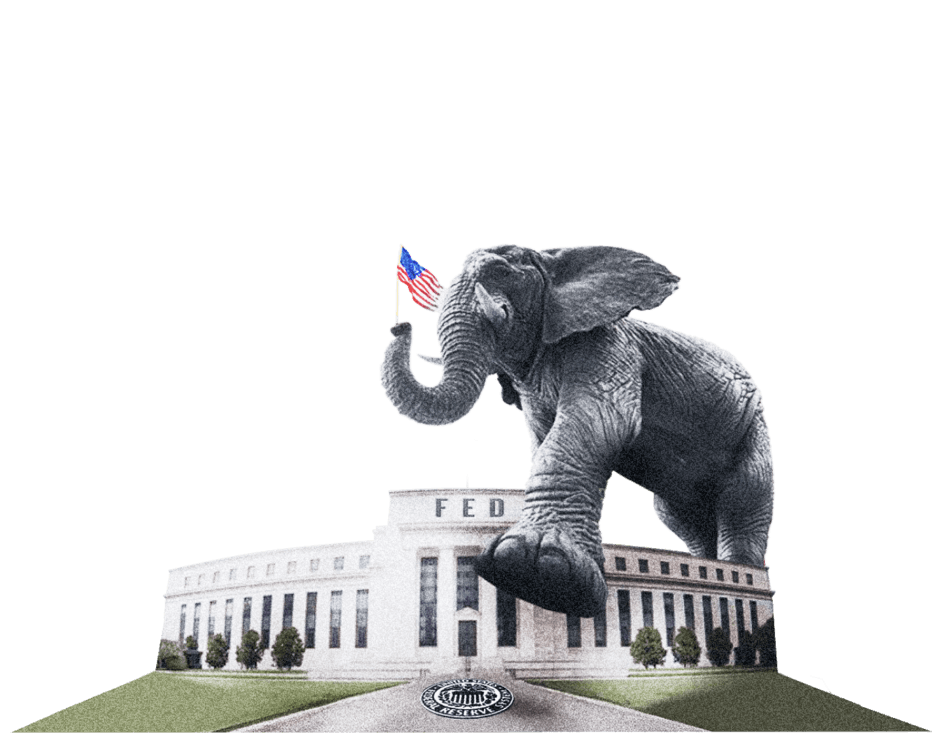

2 December - Monetary Policy

Can political interference undermine the Fed's independence and credibility?

4 December - European Autonomy

Why Europe’s autonomy agenda is becoming a powerful catalyst for new investment cycles and sector-level opportunities.

9 December - China

Innovation, policy resets, and strategic resilience redefine China's path to global leadership.

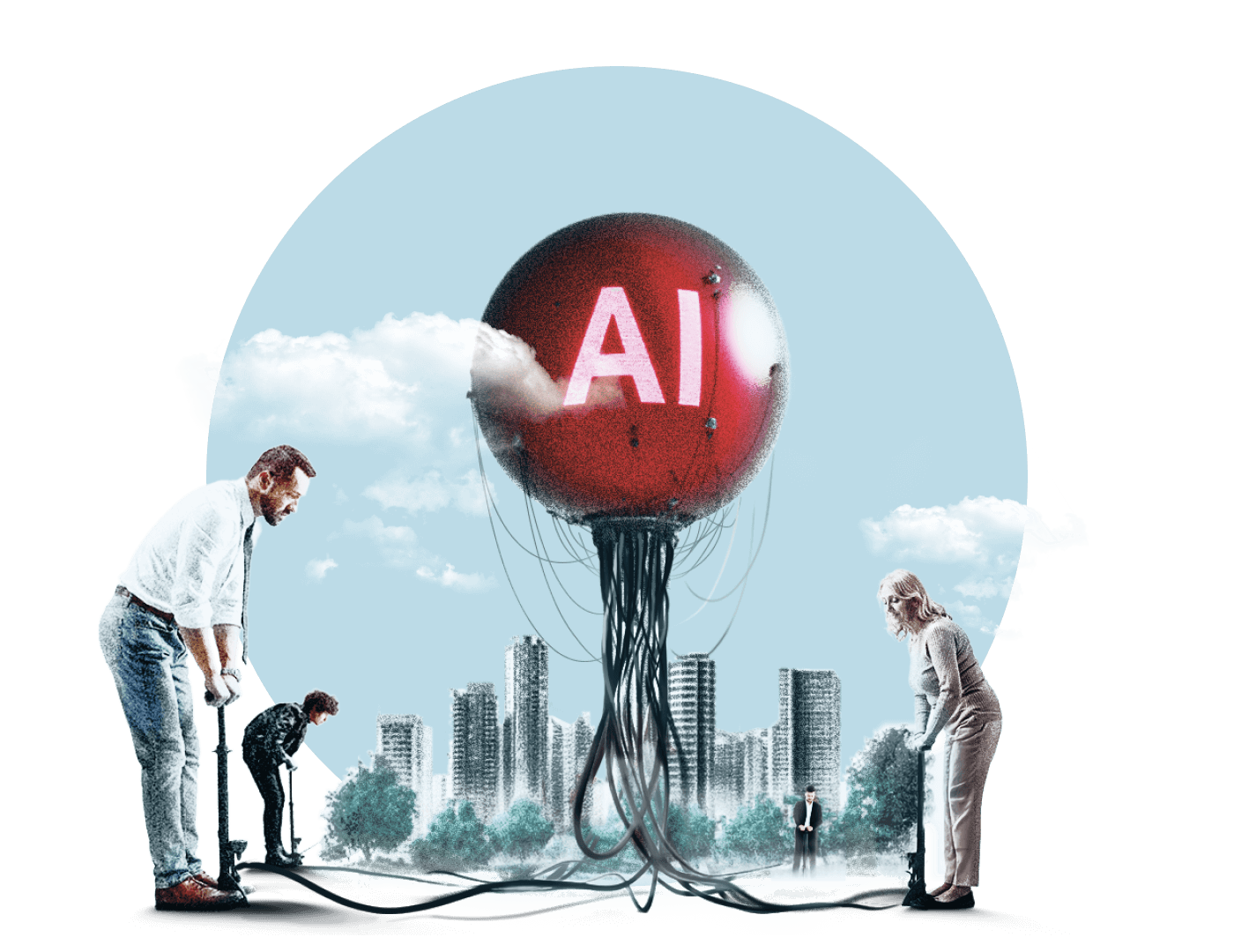

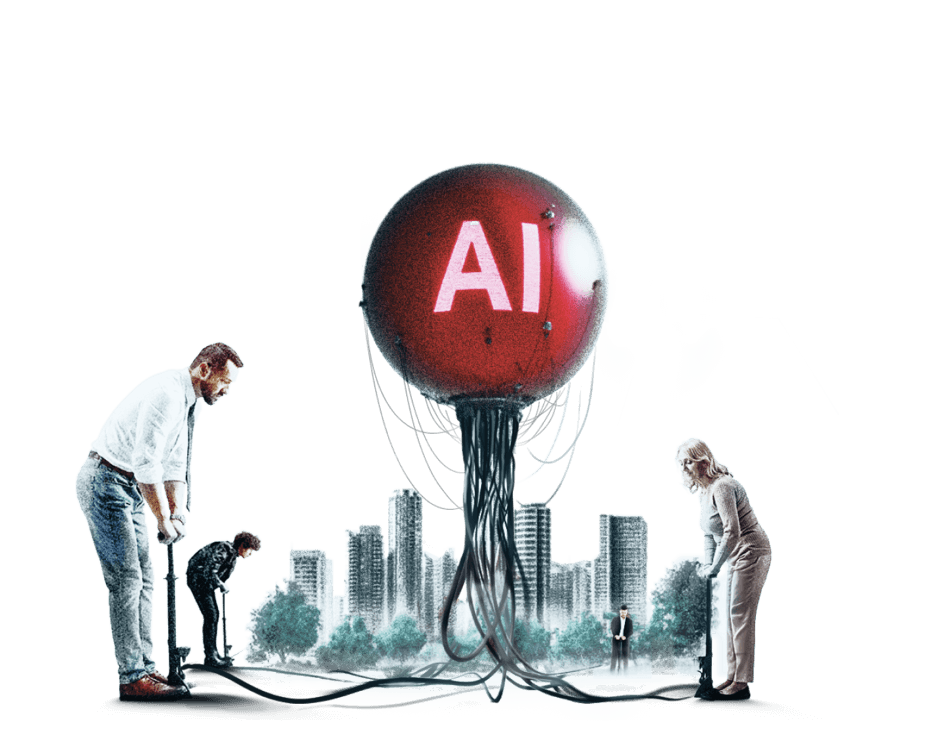

10 December - AI Bubble

AI is reshaping industries at record speed, but is this boom a bubble – or the start of a lasting transformation?

11 December - Electrification

What role will AI play in the electricity revolution?

16 December - Healthcare

With policy clarity returning, innovation accelerating and M&A heating up, is biotech poised for a powerful new growth phase?

17 December - Credit

While private credit and high yield markets will continue to offer opportunities in 2026, rigorous selection becomes essential for investors.

18 December - Gold

Safe haven, inflation hedge, diversifier, or conviction asset – what role does gold play today?

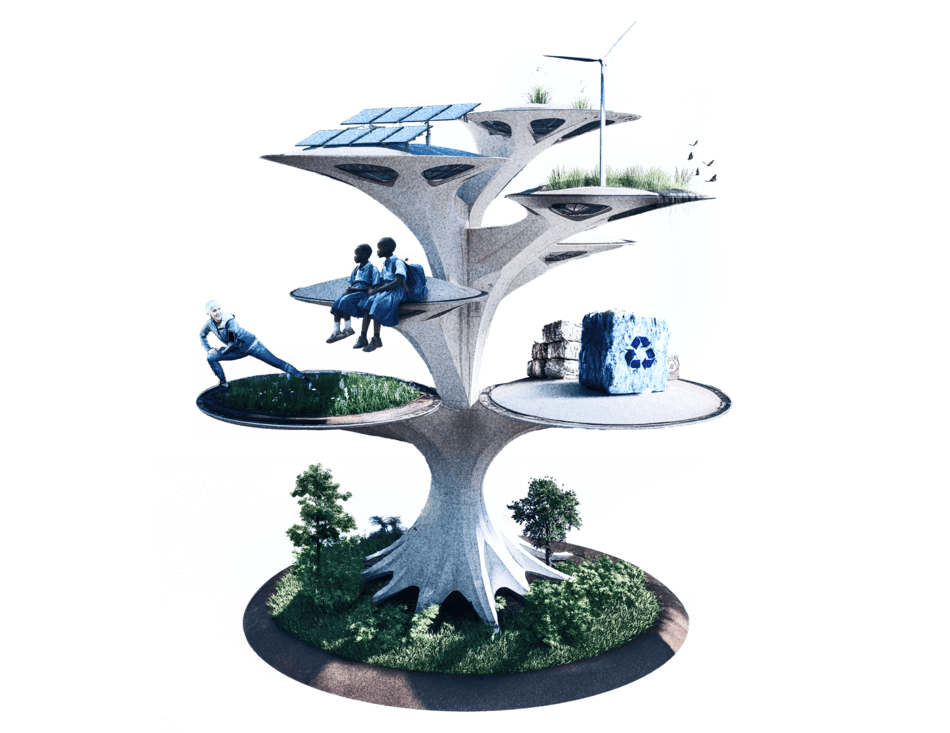

23 December - Impact Investing

Impact investing can align tangible outcomes with financial outcomes, potentially a path to restoring confidence in sustainable finance.

24 December - Asset Allocation

As AI capex intensifies, China accelerates and opportunities broaden across regions, how should investors approach portfolio construction for 2026?